Note

Go to the end to download the full example code.

Buffer-Stock Consumption Extension#

This example implements the buffer-stock consumption extension from Section 3.9.4 of Macroeconomics from the Bottom-up, replacing the baseline mean-field MPC with an individual adaptive rule based on buffer-stock saving theory.

Key Equations#

Buffer-Stock MPC (Equation 3.20):

Where: - \(h\) is the desired savings-income ratio - \(g_t = W_t / W_{t-1} - 1\) is the income growth rate - \(d_t = S_t / W_{t-1} - h\) is the divergence from desired ratio

Fresh Start Formula (just re-employed):

This example demonstrates:

Defining replacement events with

@event(replace=...)to swap pipeline behaviorHow the buffer-stock MPC differs from the baseline mean-field rule

Fitting heavy-tailed distributions (Singh-Maddala, Dagum, GB2) to wealth data

CCDF plotting on log-log axes (Figure 3.8 from the book)

- For detailed validation with bounds and statistical annotations, run:

python -m validation.scenarios.buffer_stock

Import Dependencies#

We import BAM Engine and the decorators needed to define custom components.

import bamengine as bam

from bamengine import Float, event, ops, role

from extensions.rnd import RND_EVENTS, RnD

Define Custom Role: BufferStock#

The BufferStock role tracks previous-period income and the computed MPC (propensity) for each household.

Define Replacement Events#

Two events replace the baseline consumption logic.

@event(replace=...) removes the original event from the pipeline and

inserts the new one in its place.

@event(replace="consumers_calc_propensity")

class ConsumersCalcBufferStockPropensity:

"""Compute individual MPC using buffer-stock adaptive rule.

Three cases:

1. Normal (both incomes positive): Full Eq. 3.20

2. Fresh start (just re-employed): c = 1 - h + S/W

3. Unemployed (no income): c = 1/h (gradual savings drawdown)

"""

def execute(self, sim: bam.Simulation) -> None:

con = sim.get_role("Consumer")

buf = sim.get_role("BufferStock")

income = con.income

prev_income = buf.prev_income

savings = con.savings

h = sim.buffer_stock_h

normal = (prev_income > 0) & (income > 0)

fresh = (prev_income <= 0) & (income > 0)

c = ops.full(len(income), 1 / h) # default: c=1/h (unemployed drawdown)

if ops.any(normal):

g = income[normal] / prev_income[normal] - 1.0

g = ops.maximum(g, -0.99) # g=-1.0 leads to singularity, so cap at -0.99

d = savings[normal] / prev_income[normal] - h

c[normal] = 1.0 + (d - h * g) / (1.0 + g)

if ops.any(fresh):

c[fresh] = 1.0 - h + savings[fresh] / income[fresh]

c = ops.maximum(c, 0.0)

ops.assign(buf.propensity, c)

@event(replace="consumers_decide_income_to_spend")

class ConsumersDecideBufferStockSpending:

"""Allocate spending budget using buffer-stock MPC.

Employed: budget = c * income

Unemployed: budget = c * savings

"""

def execute(self, sim: bam.Simulation) -> None:

con = sim.get_role("Consumer")

buf = sim.get_role("BufferStock")

c = buf.propensity

income = con.income

savings = con.savings

employed = income > 0

budget = ops.where(employed, c * income, c * savings)

budget = ops.minimum(budget, savings + income)

budget = ops.maximum(budget, 0.0)

ops.assign(buf.prev_income, income)

ops.assign(con.income_to_spend, budget)

new_savings = savings + income - budget

new_savings = ops.maximum(new_savings, 0.0)

ops.assign(con.savings, new_savings)

con.income.fill(0.0)

Attach Extensions#

use_role() accepts n_agents for non-firm roles (e.g., household-level).

use_events() applies pipeline hooks (after/before/replace) from event classes.

def attach_extensions(sim):

"""Attach BufferStock + RnD roles and apply extension events to pipeline."""

sim.use_role(BufferStock, n_agents=sim.n_households)

sim.use_role(RnD)

sim.use_events(

ConsumersCalcBufferStockPropensity,

ConsumersDecideBufferStockSpending,

*RND_EVENTS,

)

Initialize and Run#

Buffer-stock parameter h controls the desired savings-income ratio.

We scale initial conditions by K=100,000 so the wealth CCDF x-axis spans

[10,000 – 1,000,000], matching Figure 3.8 from the book.

sim = bam.Simulation.init(

# Buffer-stock specific parameters

buffer_stock_h=2.0,

# Scale initial conditions by K=100,000 so the wealth CCDF x-axis

# spans [10,000 – 1,000,000], matching Figure 3.8 from the book.

price_init=50_000, # K × 0.5 (default)

savings_init=100_000, # K × 1.0 (default)

equity_base_init=500_000, # K × 5.0 (default)

# net_worth scales automatically: 2.5 * 50,000 * 6.0 = 750,000

# Growth+ specific parameters

sigma_min=0.0,

sigma_max=0.1,

sigma_decay=-1.0,

# Seed

seed=0,

)

attach_extensions(sim)

print(f"Buffer-stock simulation: {sim.n_firms} firms, {sim.n_households} households")

print(f" buffer_stock_h = {sim.buffer_stock_h}")

results = sim.run()

print(f"Completed: {results.metadata['runtime_seconds']:.2f}s")

Buffer-stock simulation: 100 firms, 500 households

buffer_stock_h = 2.0

Completed: 12.20s

Fit Wealth Distribution#

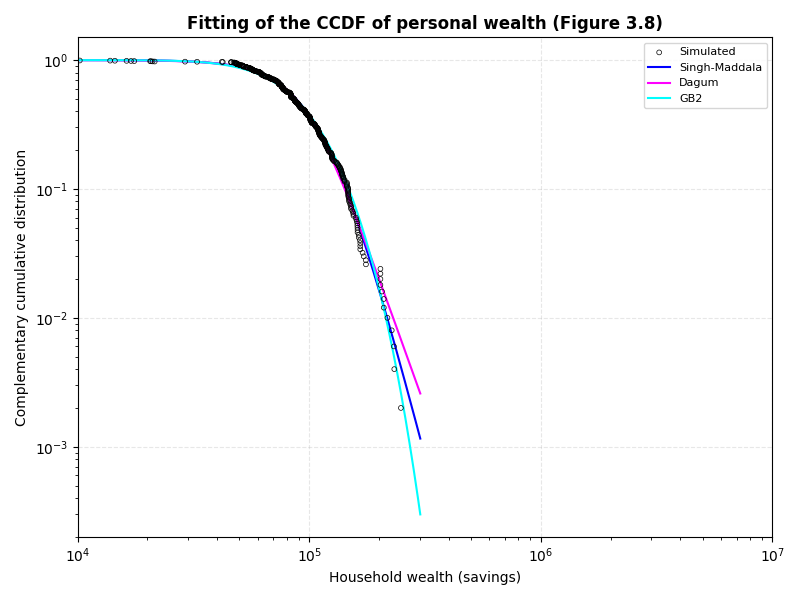

We fit the distribution of household wealth (savings) in the last period to three heavy-tailed distributions: Singh-Maddala (Burr Type XII), Dagum, and GB2 (Beta Prime). Data is normalized by its median before fitting to avoid numerical overflow in scipy’s power-law PDF evaluations (x**k overflows when x ~ 50,000+). The CCDF is scale-invariant, so we evaluate on normalized x but plot against original x.

import numpy as np

from scipy import stats as sp_stats

savings = results["Consumer.savings"]

last_period_savings = savings[-1]

fit_scale = float(np.median(last_period_savings))

norm_savings = last_period_savings / fit_scale

sm_params = sp_stats.burr12.fit(norm_savings, floc=0)

dagum_params = sp_stats.mielke.fit(norm_savings, floc=0)

gb2_params = sp_stats.betaprime.fit(norm_savings, floc=0)

Visualize Wealth CCDF (Figure 3.8)#

We plot the complementary cumulative distribution function (CCDF) of wealth on log-log axes, comparing the simulated data to the fitted distributions. The CCDF is calculated as 1 - CDF, where CDF is the cumulative distribution function.

import matplotlib.pyplot as plt

import numpy as np

fig, ax = plt.subplots(figsize=(8, 6))

sorted_wealth = ops.sort(last_period_savings)

n = len(sorted_wealth)

ccdf = 1.0 - ops.arange(1, n + 1) / n

ax.scatter(

sorted_wealth,

ccdf,

s=12,

facecolors="none",

edgecolors="black",

linewidths=0.5,

label="Simulated",

zorder=5,

)

x_range = np.linspace(sorted_wealth[0], sorted_wealth[-1], 500)

x_norm = x_range / fit_scale # normalized x for distribution evaluation

# Calculate CCDF (survival function) for each fitted distribution.

# We use .sf() instead of 1-cdf() for better numerical stability in the tail.

# Note: scipy's 'burr12' distribution is a reparameterization of the Singh-Maddala distribution.

sm_ccdf = sp_stats.burr12.sf(x_norm, *sm_params)

ax.plot(x_range, sm_ccdf, color="#0000FE", linewidth=1.5, label="Singh-Maddala")

# Note: scipy's 'mielke' distribution is a reparameterization of the Dagum distribution.

dagum_ccdf = sp_stats.mielke.sf(x_norm, *dagum_params)

ax.plot(x_range, dagum_ccdf, color="#FE00FE", linewidth=1.5, label="Dagum")

# Note: scipy's 'betaprime' distribution is a reparameterization of the GB2 distribution.

gb2_ccdf = sp_stats.betaprime.sf(x_norm, *gb2_params)

ax.plot(x_range, gb2_ccdf, color="#00FEFE", linewidth=1.5, label="GB2")

ax.set_xscale("log")

ax.set_yscale("log")

ax.set_xlim(1e4, 1e7)

ax.legend(fontsize=8)

ax.set_title("Fitting of the CCDF of personal wealth (Figure 3.8)", fontweight="bold")

ax.set_xlabel("Household wealth (savings)")

ax.set_ylabel("Complementary cumulative distribution")

ax.grid(True, linestyle="--", alpha=0.3)

plt.tight_layout()

plt.show()

Alternative: Extension Bundle#

The above example defines all buffer-stock components inline for educational

purposes. For convenience, the pre-built BUFFER_STOCK bundle activates

everything in one call:

from extensions.rnd import RND

from extensions.buffer_stock import BUFFER_STOCK, BUFFER_STOCK_COLLECT

sim = bam.Simulation.init(seed=0)

sim.use(RND)

sim.use(BUFFER_STOCK)

results = sim.run(collect=BUFFER_STOCK_COLLECT)

Total running time of the script: (0 minutes 12.663 seconds)