Note

Go to the end to download the full example code.

Growth+ Model Extension#

This example implements the Growth+ extension from chapter 3.8 of Macroeconomics from the Bottom-up, demonstrating endogenous productivity growth based on R&D investment.

Key Equations#

Productivity Evolution (Equation 3.15):

Where \(z_t \sim \text{Exponential}(\mu)\) represents the productivity increment drawn from an exponential distribution with scale parameter \(\mu\).

R&D Intensity (expected productivity gain):

This example demonstrates:

Defining custom roles with the

@roledecoratorCreating custom events with the

@eventdecoratorUsing pipeline hooks via

@event(after=...)for declarative event positioningAttaching custom roles to simulations via

sim.use_role()

- For detailed validation with bounds and statistical annotations, run:

python -m validation.scenarios.growth_plus

Import Dependencies#

We import BAM Engine and the decorators needed to define custom components.

import bamengine as bam

from bamengine import Float, event, ops, role

Define Custom Role: RnD#

The RnD role tracks R&D-related state for each firm.

Define Custom Events#

Three events implement the Growth+ mechanism.

@event(name="firms_compute_rnd_intensity", after="firms_validate_debt_commitments")

class FirmsComputeRnDIntensity:

"""Compute R&D share and intensity for firms."""

def execute(self, sim: bam.Simulation) -> None:

bor = sim.get_role("Borrower")

prod = sim.get_role("Producer")

emp = sim.get_role("Employer")

rnd = sim.get_role("RnD")

sigma_min, sigma_max, sigma_decay = (

sim.sigma_min,

sim.sigma_max,

sim.sigma_decay,

)

eps = 1e-10

safe_net_worth = ops.where(ops.greater(bor.net_worth, eps), bor.net_worth, eps)

fragility = ops.divide(emp.wage_bill, safe_net_worth)

ops.assign(rnd.fragility, fragility)

decay_factor = ops.exp(ops.multiply(sigma_decay, fragility))

sigma = ops.add(sigma_min, ops.multiply(sigma_max - sigma_min, decay_factor))

sigma = ops.where(ops.greater(bor.net_profit, 0.0), sigma, 0.0)

ops.assign(rnd.sigma, sigma)

revenue = ops.multiply(prod.price, prod.production)

safe_revenue = ops.where(ops.greater(revenue, eps), revenue, eps)

mu = ops.divide(ops.multiply(sigma, bor.net_profit), safe_revenue)

mu = ops.where(ops.greater(mu, 0.0), mu, 0.0)

ops.assign(rnd.rnd_intensity, mu)

@event(after="firms_compute_rnd_intensity")

class FirmsApplyProductivityGrowth:

"""Apply productivity growth based on R&D."""

def execute(self, sim: bam.Simulation) -> None:

prod = sim.get_role("Producer")

rnd = sim.get_role("RnD")

z = ops.zeros(sim.n_firms)

active = ops.greater(rnd.rnd_intensity, 0.0)

if ops.any(active):

z[active] = sim.rng.exponential(scale=rnd.rnd_intensity[active])

ops.assign(rnd.productivity_increment, z)

ops.assign(prod.labor_productivity, ops.add(prod.labor_productivity, z))

@event(after="firms_apply_productivity_growth")

class FirmsDeductRnDExpenditure:

"""Adjust net profit for R&D expenditure."""

def execute(self, sim: bam.Simulation) -> None:

bor = sim.get_role("Borrower")

rnd = sim.get_role("RnD")

new_net_profit = ops.multiply(bor.net_profit, ops.subtract(1.0, rnd.sigma))

ops.assign(bor.net_profit, new_net_profit)

Initialize Simulation#

Create a simulation using extra parameters for the Growth+ extension and attach the RnD role and events.

sim = bam.Simulation.init(

# Growth+ parameters

sigma_min=0.0,

sigma_max=0.1,

sigma_decay=-1.0,

# Seed

seed=0,

)

sim.use_role(RnD)

sim.use_events(

FirmsComputeRnDIntensity, FirmsApplyProductivityGrowth, FirmsDeductRnDExpenditure

)

print(f"Growth+ simulation: {sim.n_firms} firms, {sim.n_households} households")

Growth+ simulation: 100 firms, 500 households

Run Simulation#

Collect per-agent data with capture timing matching the validation scenario.

COLLECT_CONFIG = {

"Producer": ["production", "labor_productivity", "price", "inventory"],

"Worker": ["wage", "employed"],

"Employer": ["n_vacancies"],

"Borrower": ["net_worth"],

"Consumer": ["income_to_spend"],

"LoanBook": ["principal", "rate", "source_ids"],

"capture_timing": {

# Capture wages after workers receive them

"Worker.wage": "firms_run_production",

# Employment status after production completes

"Worker.employed": "firms_run_production",

# Production output after firms run production

"Producer.production": "firms_run_production",

# Productivity after R&D growth is applied (captures the increment)

"Producer.labor_productivity": "firms_apply_productivity_growth",

# Price after planning phase sets it

"Producer.price": "firms_plan_price",

# Inventory after consumers finish purchasing

"Producer.inventory": "consumers_finalize_purchases",

# Vacancies right after firms decide them

"Employer.n_vacancies": "firms_decide_vacancies",

# Net worth after production (before bankruptcy may reset it)

"Borrower.net_worth": "firms_run_production",

# Consumer budget after it's decided

"Consumer.income_to_spend": "consumers_decide_income_to_spend",

# Loan data after credit market matching

"LoanBook.principal": "credit_market_round",

"LoanBook.rate": "credit_market_round",

"LoanBook.source_ids": "credit_market_round",

},

}

results = sim.run(collect=COLLECT_CONFIG)

print(f"Completed: {results.metadata['runtime_seconds']:.2f}s")

Completed: 12.71s

Compute Metrics#

Compute macro indicators and financial dynamics from the simulation results.

import numpy as np

burn_in = 500

n_periods = sim.n_periods

EPS = 1e-9

# Extract raw data from results

avg_price = results["Economy.avg_price"]

production = results.get("Producer", "production")

productivity = results.get("Producer", "labor_productivity")

prices = results.get("Producer", "price")

inventory = results.get("Producer", "inventory")

wages = results.get("Worker", "wage")

employed_arr = results.get("Worker", "employed")

n_vacancies = results.get("Employer", "n_vacancies")

net_worth = results.get("Borrower", "net_worth")

consumer_budget = results.get("Consumer", "income_to_spend")

loan_principals = results["LoanBook.principal"]

loan_rates = results["LoanBook.rate"]

bankruptcies = np.array(results["Economy.n_firm_bankruptcies"])

# Compute total production (GDP)

gdp = ops.sum(production, axis=1)

# Unemployment rate

unemployment = 1 - ops.mean(employed_arr.astype(float), axis=1)

# Log GDP

log_gdp = ops.log(gdp + 1e-10)

# Inflation

inflation = results["Economy.inflation"]

# Average wage for employed workers

employed_wages_sum = ops.sum(ops.where(employed_arr, wages, 0.0), axis=1)

employed_count = ops.sum(employed_arr, axis=1)

avg_wage = ops.where(

ops.greater(employed_count, 0),

ops.divide(employed_wages_sum, employed_count),

0.0,

)

# Real wage

real_wage = ops.divide(avg_wage, avg_price)

# Production-weighted average productivity

weighted_prod = ops.sum(ops.multiply(productivity, production), axis=1)

avg_productivity = ops.divide(weighted_prod, gdp)

# Wage inflation for Phillips curve

wage_inflation = ops.divide(

avg_wage[1:] - avg_wage[:-1],

ops.where(ops.greater(avg_wage[:-1], 0), avg_wage[:-1], 1.0),

)

# GDP growth for Okun curve

gdp_growth = ops.divide(gdp[1:] - gdp[:-1], gdp[:-1])

# Unemployment growth for Okun curve

unemployment_growth = ops.divide(

unemployment[1:] - unemployment[:-1],

ops.where(ops.greater(unemployment[:-1], 0), unemployment[:-1], 1.0),

)

# Vacancy rate

total_vacancies = ops.sum(n_vacancies, axis=1)

vacancy_rate = ops.divide(total_vacancies, sim.n_households)

# Final period firm production

prod = sim.get_role("Producer")

final_production = prod.production.copy()

# Correlations

phillips_corr = np.corrcoef(unemployment[burn_in:], wage_inflation[burn_in - 1 :])[0, 1]

okun_corr = np.corrcoef(unemployment_growth[burn_in - 1 :], gdp_growth[burn_in - 1 :])[

0, 1

]

beveridge_corr = np.corrcoef(unemployment[burn_in:], vacancy_rate[burn_in:])[0, 1]

prod_growth = (avg_productivity[-1] - avg_productivity[burn_in]) / avg_productivity[

burn_in

]

# Recession detection

def detect_recessions(

log_gdp_series, window=5, threshold=0.02, min_gap=10, min_duration=15

):

"""Detect recessions as sustained drawdowns from smoothed GDP peaks."""

kernel = np.ones(window) / window

smoothed = np.convolve(log_gdp_series, kernel, mode="same")

running_max = np.maximum.accumulate(smoothed)

drawdown = running_max - smoothed

mask = drawdown > threshold

if np.any(mask):

# Bridge short gaps between nearby recessions

padded = np.concatenate([[False], mask, [False]])

starts = np.where(padded[1:] & ~padded[:-1])[0]

ends = np.where(~padded[1:] & padded[:-1])[0]

for i in range(len(ends) - 1):

if starts[i + 1] - ends[i] < min_gap:

mask[ends[i] : starts[i + 1]] = True

# Remove recessions shorter than min_duration

padded = np.concatenate([[False], mask, [False]])

starts = np.where(padded[1:] & ~padded[:-1])[0]

ends = np.where(~padded[1:] & padded[:-1])[0]

for s, e in zip(starts, ends, strict=True):

if e - s < min_duration:

mask[s:e] = False

return mask

recession_mask = detect_recessions(log_gdp)

# Financial dynamics

real_interest_rate = np.zeros(n_periods)

for t in range(n_periods):

principals_t = loan_principals[t]

rates_t = loan_rates[t]

if len(principals_t) > 0 and np.sum(principals_t) > 0:

weighted_nominal = float(np.sum(rates_t * principals_t) / np.sum(principals_t))

else:

weighted_nominal = sim.r_bar

real_interest_rate[t] = weighted_nominal - inflation[t]

total_wage_bill = ops.sum(wages * employed_arr.astype(float), axis=1)

total_net_worth = ops.sum(net_worth, axis=1)

safe_total_nw = ops.where(ops.greater(total_net_worth, EPS), total_net_worth, EPS)

financial_fragility = ops.divide(total_wage_bill, safe_total_nw)

safe_gdp = ops.where(ops.greater(gdp, EPS), gdp, EPS)

total_demand = ops.sum(consumer_budget, axis=1)

market_clearing_price = ops.divide(total_demand, safe_gdp)

price_ratio = ops.divide(avg_price, market_clearing_price)

# Price dispersion: production-weighted CV

safe_prod = np.where(production > 0, production, 0.0)

prod_sum = np.sum(safe_prod, axis=1, keepdims=True)

prod_weights = safe_prod / np.where(prod_sum > EPS, prod_sum, EPS)

weighted_price_mean = np.sum(prod_weights * prices, axis=1, keepdims=True)

weighted_price_var = np.sum(prod_weights * (prices - weighted_price_mean) ** 2, axis=1)

weighted_price_std = np.sqrt(np.maximum(weighted_price_var, 0.0))

w_mean_flat = weighted_price_mean.squeeze()

safe_w_mean = np.where(w_mean_flat > EPS, w_mean_flat, EPS)

price_dispersion = weighted_price_std / safe_w_mean

# Equity dispersion: std / abs(mean) with EPS

nw_mean = ops.mean(net_worth, axis=1)

equity_dispersion = ops.divide(

ops.std(net_worth, axis=1),

ops.where(ops.greater(np.abs(nw_mean), EPS), np.abs(nw_mean), EPS),

)

# Sales dispersion: price * (production - inventory)

qty_sold = np.subtract(production, inventory)

sales = ops.multiply(prices, qty_sold)

sales_mean = ops.mean(sales, axis=1)

sales_dispersion = ops.divide(

ops.std(sales, axis=1),

ops.where(ops.greater(np.abs(sales_mean), EPS), np.abs(sales_mean), EPS),

)

# Output growth rates (aggregate GDP, post-burn-in)

gdp_after_burnin = gdp[burn_in:]

output_growth_rates = np.diff(gdp_after_burnin) / gdp_after_burnin[:-1]

# Net worth growth rates (final two periods, valid firms)

nw_prev = net_worth[-2]

nw_final = net_worth[-1]

valid_firms = (nw_prev > 0) & (nw_final > 0)

nw_prev_valid = nw_prev[valid_firms]

nw_final_valid = nw_final[valid_firms]

networth_growth_rates = (nw_final_valid - nw_prev_valid) / nw_prev_valid

# Exclude re-entries (bankruptcy respawns cause |growth| >> 100%)

reentry_mask = np.abs(networth_growth_rates) <= 1.0

networth_growth_rates = networth_growth_rates[reentry_mask]

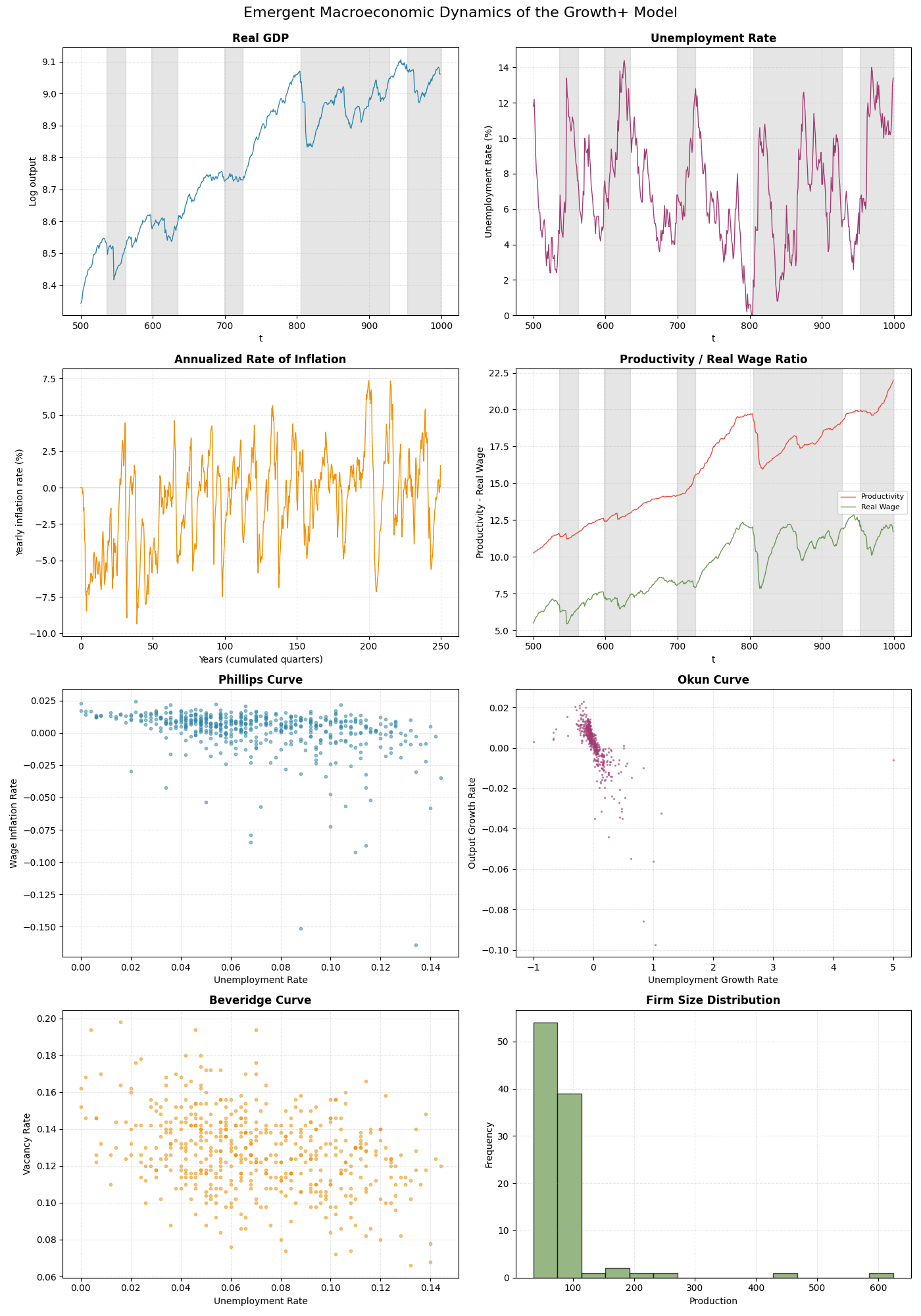

print(f"\nKey metrics (after {burn_in}-period burn-in):")

print(f" Unemployment: {np.mean(unemployment[burn_in:]) * 100:.1f}%")

print(f" Inflation: {np.mean(inflation[burn_in:]) * 100:.1f}%")

print(f" Productivity growth: {prod_growth * 100:.0f}%")

print(f" Phillips correlation: {phillips_corr:.2f}")

print(f" Okun correlation: {okun_corr:.2f}")

print(f" Beveridge correlation: {beveridge_corr:.2f}")

Key metrics (after 500-period burn-in):

Unemployment: 6.6%

Inflation: 0.3%

Productivity growth: 106%

Phillips correlation: -0.34

Okun correlation: -0.56

Beveridge correlation: -0.23

Visualize Results (Macro Dynamics)#

4x2 figure showing time series with recession bands and macroeconomic curves.

import matplotlib.pyplot as plt

def add_recession_bands(ax, periods, mask):

"""Shade recession episodes on a time-series axis."""

if not np.any(mask):

return

in_rec = False

start_idx = 0

for i, is_rec in enumerate(mask):

if is_rec and not in_rec:

start_idx = i

in_rec = True

elif not is_rec and in_rec:

ax.axvspan(periods[start_idx], periods[i - 1], alpha=0.2, color="gray")

in_rec = False

if in_rec:

ax.axvspan(periods[start_idx], periods[-1], alpha=0.2, color="gray")

periods = ops.arange(burn_in, n_periods)

fig, axes = plt.subplots(4, 2, figsize=(14, 20))

fig.suptitle(

"Emergent Macroeconomic Dynamics of the Growth+ Model", fontsize=16, y=0.995

)

# Panel (0,0): Log Real GDP

ax = axes[0, 0]

add_recession_bands(ax, periods, recession_mask[burn_in:])

ax.plot(periods, log_gdp[burn_in:], linewidth=1, color="#2E86AB")

ax.set_title("Real GDP", fontsize=12, fontweight="bold")

ax.set_ylabel("Log output")

ax.set_xlabel("t")

ax.grid(True, linestyle="--", alpha=0.3)

# Panel (0,1): Unemployment Rate

ax = axes[0, 1]

add_recession_bands(ax, periods, recession_mask[burn_in:])

ax.plot(periods, unemployment[burn_in:] * 100, linewidth=1, color="#A23B72")

ax.set_title("Unemployment Rate", fontsize=12, fontweight="bold")

ax.set_ylabel("Unemployment Rate (%)")

ax.set_xlabel("t")

ax.set_ylim(bottom=0)

ax.grid(True, linestyle="--", alpha=0.3)

# Panel (1,0): Inflation Rate (all periods, cumulated years)

ax = axes[1, 0]

years = ops.arange(0, n_periods) / 4

ax.plot(years, inflation * 100, linewidth=1, color="#F18F01")

ax.axhline(0, color="black", linestyle="-", alpha=0.3, linewidth=0.5)

ax.set_title("Annualized Rate of Inflation", fontsize=12, fontweight="bold")

ax.set_ylabel("Yearly inflation rate (%)")

ax.set_xlabel("Years (cumulated quarters)")

ax.grid(True, linestyle="--", alpha=0.3)

# Panel (1,1): Productivity and Real Wage

ax = axes[1, 1]

add_recession_bands(ax, periods, recession_mask[burn_in:])

ax.plot(

periods,

avg_productivity[burn_in:],

linewidth=1,

color="#E74C3C",

label="Productivity",

)

ax.plot(periods, real_wage[burn_in:], linewidth=1, color="#6A994E", label="Real Wage")

ax.set_title("Productivity / Real Wage Ratio", fontsize=12, fontweight="bold")

ax.set_ylabel("Productivity - Real Wage")

ax.set_xlabel("t")

ax.legend(loc="center right", fontsize=8)

ax.grid(True, linestyle="--", alpha=0.3)

# Panel (2,0): Phillips Curve

ax = axes[2, 0]

ax.scatter(

unemployment[burn_in:],

wage_inflation[burn_in - 1 :],

s=10,

alpha=0.5,

color="#2E86AB",

)

ax.set_title("Phillips Curve", fontsize=12, fontweight="bold")

ax.set_xlabel("Unemployment Rate")

ax.set_ylabel("Wage Inflation Rate")

ax.grid(True, linestyle="--", alpha=0.3)

# Panel (2,1): Okun Curve

ax = axes[2, 1]

ax.scatter(

unemployment_growth[burn_in - 1 :],

gdp_growth[burn_in - 1 :],

s=2,

alpha=0.5,

color="#A23B72",

)

ax.set_title("Okun Curve", fontsize=12, fontweight="bold")

ax.set_xlabel("Unemployment Growth Rate")

ax.set_ylabel("Output Growth Rate")

ax.grid(True, linestyle="--", alpha=0.3)

# Panel (3,0): Beveridge Curve

ax = axes[3, 0]

ax.scatter(

unemployment[burn_in:], vacancy_rate[burn_in:], s=10, alpha=0.5, color="#F18F01"

)

ax.set_title("Beveridge Curve", fontsize=12, fontweight="bold")

ax.set_xlabel("Unemployment Rate")

ax.set_ylabel("Vacancy Rate")

ax.grid(True, linestyle="--", alpha=0.3)

# Panel (3,1): Firm Size Distribution

ax = axes[3, 1]

ax.hist(final_production, bins=15, edgecolor="black", alpha=0.7, color="#6A994E")

ax.set_title("Firm Size Distribution", fontsize=12, fontweight="bold")

ax.set_xlabel("Production")

ax.set_ylabel("Frequency")

ax.grid(True, linestyle="--", alpha=0.3)

plt.tight_layout()

plt.show()

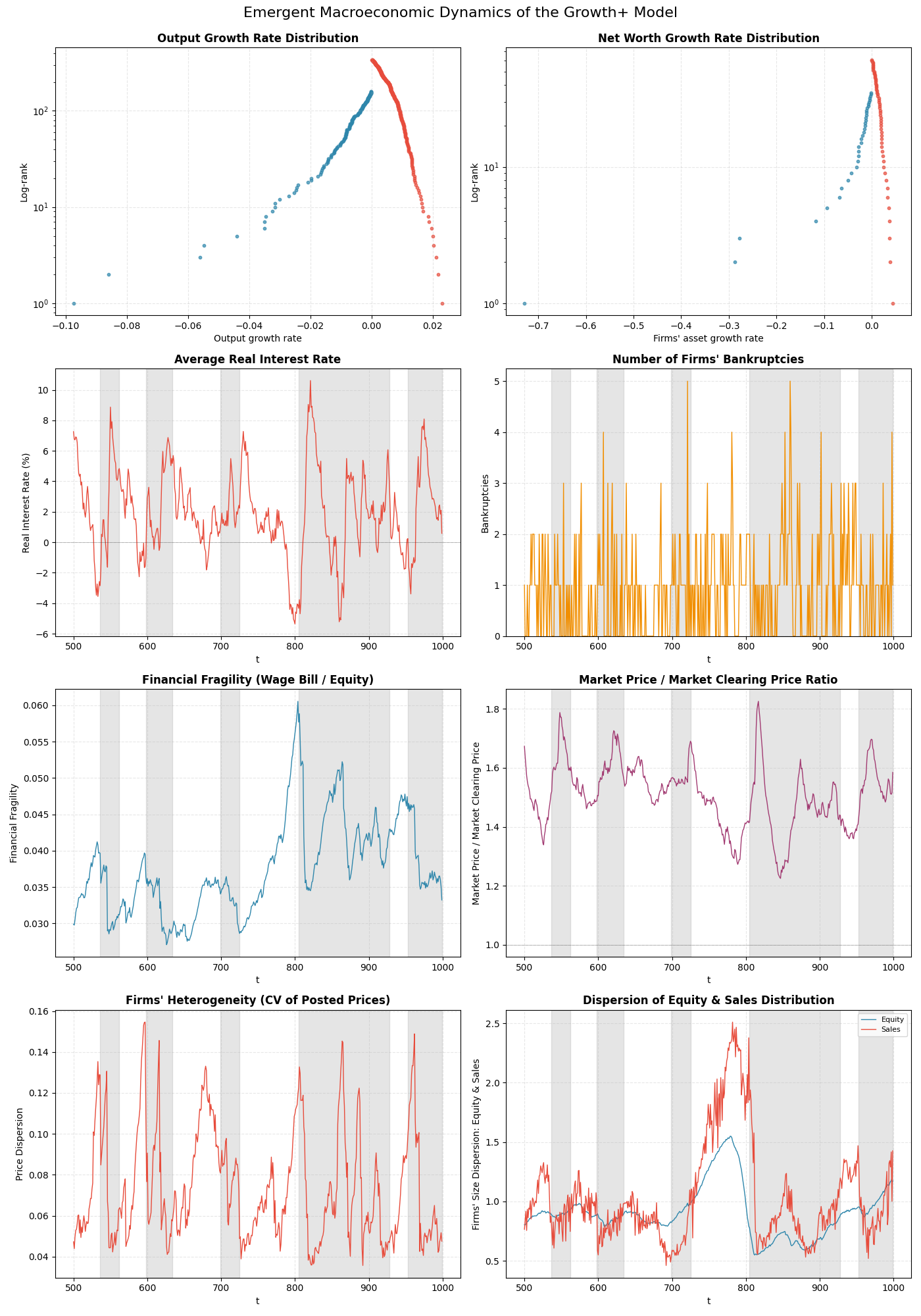

Visualize Financial Dynamics#

4x2 figure showing growth distributions, interest rates, and financial indicators.

fig2, axes2 = plt.subplots(4, 2, figsize=(14, 20))

fig2.suptitle(

"Emergent Macroeconomic Dynamics of the Growth+ Model", fontsize=16, y=0.995

)

# Panel (0,0): Output Growth Rate Distribution (log-rank)

ax = axes2[0, 0]

filtered = output_growth_rates[np.isfinite(output_growth_rates)]

negative = filtered[filtered < 0]

positive = filtered[filtered >= 0]

neg_sorted = np.sort(negative)

neg_ranks = np.arange(1, len(neg_sorted) + 1)

pos_sorted = np.sort(positive)[::-1]

pos_ranks = np.arange(1, len(pos_sorted) + 1)

ax.scatter(neg_sorted, neg_ranks, s=10, alpha=0.7, color="#2E86AB")

ax.scatter(pos_sorted, pos_ranks, s=10, alpha=0.7, color="#E74C3C")

ax.set_yscale("log")

ax.set_title("Output Growth Rate Distribution", fontsize=12, fontweight="bold")

ax.set_xlabel("Output growth rate")

ax.set_ylabel("Log-rank")

ax.grid(True, linestyle="--", alpha=0.3)

# Panel (0,1): Net Worth Growth Rate Distribution (log-rank)

ax = axes2[0, 1]

filtered = networth_growth_rates[np.isfinite(networth_growth_rates)]

negative = filtered[filtered < 0]

positive = filtered[filtered >= 0]

neg_sorted = np.sort(negative)

neg_ranks = np.arange(1, len(neg_sorted) + 1)

pos_sorted = np.sort(positive)[::-1]

pos_ranks = np.arange(1, len(pos_sorted) + 1)

ax.scatter(neg_sorted, neg_ranks, s=10, alpha=0.7, color="#2E86AB")

ax.scatter(pos_sorted, pos_ranks, s=10, alpha=0.7, color="#E74C3C")

ax.set_yscale("log")

ax.set_title("Net Worth Growth Rate Distribution", fontsize=12, fontweight="bold")

ax.set_xlabel("Firms' asset growth rate")

ax.set_ylabel("Log-rank")

ax.grid(True, linestyle="--", alpha=0.3)

# Panel (1,0): Real Interest Rate

ax = axes2[1, 0]

add_recession_bands(ax, periods, recession_mask[burn_in:])

ax.plot(periods, real_interest_rate[burn_in:] * 100, linewidth=1, color="#E74C3C")

ax.axhline(0, color="black", linestyle="-", alpha=0.3, linewidth=0.5)

ax.set_title("Average Real Interest Rate", fontsize=12, fontweight="bold")

ax.set_ylabel("Real Interest Rate (%)")

ax.set_xlabel("t")

ax.grid(True, linestyle="--", alpha=0.3)

# Panel (1,1): Firm Bankruptcies

ax = axes2[1, 1]

add_recession_bands(ax, periods, recession_mask[burn_in:])

ax.plot(periods, bankruptcies[burn_in:], linewidth=1, color="#F18F01")

ax.set_title("Number of Firms' Bankruptcies", fontsize=12, fontweight="bold")

ax.set_ylabel("Bankruptcies")

ax.set_xlabel("t")

ax.set_ylim(bottom=0)

ax.grid(True, linestyle="--", alpha=0.3)

# Panel (2,0): Financial Fragility

ax = axes2[2, 0]

add_recession_bands(ax, periods, recession_mask[burn_in:])

ax.plot(periods, financial_fragility[burn_in:], linewidth=1, color="#2E86AB")

ax.set_title("Financial Fragility (Wage Bill / Equity)", fontsize=12, fontweight="bold")

ax.set_ylabel("Financial Fragility")

ax.set_xlabel("t")

ax.grid(True, linestyle="--", alpha=0.3)

# Panel (2,1): Price Ratio

ax = axes2[2, 1]

add_recession_bands(ax, periods, recession_mask[burn_in:])

ax.plot(periods, price_ratio[burn_in:], linewidth=1, color="#A23B72")

ax.axhline(1, color="black", linestyle="-", alpha=0.3, linewidth=0.5)

ax.set_title(

"Market Price / Market Clearing Price Ratio", fontsize=12, fontweight="bold"

)

ax.set_ylabel("Market Price / Market Clearing Price")

ax.set_xlabel("t")

ax.grid(True, linestyle="--", alpha=0.3)

# Panel (3,0): Price Dispersion (CV)

ax = axes2[3, 0]

add_recession_bands(ax, periods, recession_mask[burn_in:])

ax.plot(periods, price_dispersion[burn_in:], linewidth=1, color="#E74C3C")

ax.set_title(

"Firms' Heterogeneity (CV of Posted Prices)", fontsize=12, fontweight="bold"

)

ax.set_ylabel("Price Dispersion")

ax.set_xlabel("t")

ax.grid(True, linestyle="--", alpha=0.3)

# Panel (3,1): Equity & Sales Dispersion

ax = axes2[3, 1]

add_recession_bands(ax, periods, recession_mask[burn_in:])

ax.plot(

periods,

equity_dispersion[burn_in:],

linewidth=1,

color="#2E86AB",

label="Equity",

)

ax.plot(

periods,

sales_dispersion[burn_in:],

linewidth=1,

color="#E74C3C",

label="Sales",

)

ax.set_title(

"Dispersion of Equity & Sales Distribution", fontsize=12, fontweight="bold"

)

ax.set_ylabel("Firms' Size Dispersion: Equity & Sales")

ax.set_xlabel("t")

ax.legend(loc="upper right", fontsize=8)

ax.grid(True, linestyle="--", alpha=0.3)

plt.tight_layout()

plt.show()

Alternative: Extension Bundle#

The above example defines all R&D components inline for educational purposes.

For convenience, the pre-built RND bundle activates everything in one call:

from extensions.rnd import RND, RND_COLLECT

sim = bam.Simulation.init(seed=0)

sim.use(RND)

results = sim.run(collect=RND_COLLECT)

Total running time of the script: (0 minutes 14.939 seconds)